The National Pension System (NPS) is a voluntary, defined contribution retirement savings scheme designed to enable subscribers to make decisions regarding their future through systematic savings during their working life.

Contents

Who can register for NPS?

The National Pension System (NPS) in India is open to various categories of individuals. Here are the main eligibility criteria:

- Citizens of India: Both residents and non-resident Indians (NRIs) can register for NPS.

- Age: Individuals aged between 18 and 70 years at the time of submitting their application can register.

- Salaried Employees: Both government and private sector employees can enroll in NPS.

- Self-Employed Individuals: Self-employed professionals and business owners can also register for NPS.

- Corporate Employees: Many companies offer NPS as part of their retirement benefits package.

There are two types of accounts within NPS:

- Tier I Account: This is the primary retirement account with restrictions on withdrawals and tax benefits.

- Tier II Account: This is a voluntary savings account with more flexibility but without the same tax benefits as Tier I.

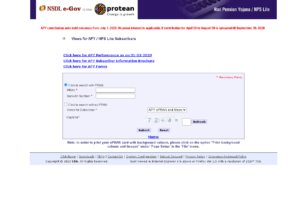

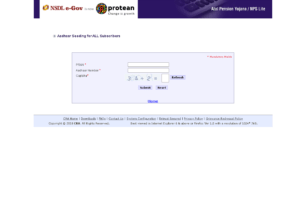

NPS Online Subscriber Registration

To register for the National Pension System (NPS) online in India, follow these steps:

Steps for Online Registration:

- Visit the Official Website: Go to the NPS Trust website or the eNPS portal at CAMS & NSDL

- New Registration: Click on the “Registration” tab and select the appropriate option, such as “Individual Subscriber Registration.”

- Choose Your Citizenship: Select your citizenship (Indian or Non-Resident Indian).

- Personal Details: Fill in your personal details, including your full name, date of birth, email ID, and mobile number.

- Choose a Permanent Retirement Account Number (PRAN): If you do not have a PRAN, select the option to generate a new PRAN.

- KYC Verification:

- Aadhaar-Based KYC: Use your Aadhaar number for KYC verification. An OTP will be sent to your registered mobile number for authentication.

- PAN-Based KYC: If using PAN, you will need to provide additional details, including your bank account information. The bank must be an empaneled POP (Point of Presence) with NPS for KYC verification.

- Bank Details: Enter your bank account details for linking with NPS.

- Nomination Details: Provide details of your nominee(s) for the NPS account.

- Choose Your Pension Fund Manager (PFM): Select a Pension Fund Manager from the list of available managers. You can also choose your investment option (active or auto choice).

- Upload Documents: Upload a scanned copy of your photograph, signature, and other required documents (such as Aadhaar, PAN, etc.).

- Payment of Initial Contribution: Make the initial contribution to your NPS account. The minimum amount for the initial contribution is ₹500 for a Tier I account.

- Submit the Form: Review all the details, ensure everything is correct, and submit the form.

- PRAN Generation: Once your application is processed and verified, you will receive your PRAN (Permanent Retirement Account Number).

Key Points to Remember:

- Ensure that all details provided match the documents you are submitting for KYC.

- Keep your Aadhaar number and registered mobile number handy for OTP verification if using Aadhaar for KYC.

- Make sure your bank account is active and has sufficient funds for the initial contribution.

Post Registration:

- You will receive a PRAN card and a welcome kit containing details of your NPS account.

- You can manage your NPS account online through the eNPS portal, including making contributions, checking statements, and updating personal details.

NPS Calculator

The NPS calculator is a tool that helps you estimate the potential retirement corpus and monthly pension you can receive based on your contributions to the National Pension System. Here’s how you can use the NPS calculator:

Steps to Use the NPS Calculator:

- Access the Calculator:

- You can use online NPS calculators available on various financial websites or the official NPS website. One such calculator is available on the NPS Trust website or directly at NSDL NPS Calculator.

- Enter Your Details:

- Date of Birth/Age: Enter your current age.

- Investment Amount: Enter the amount you plan to invest each month or annually.

- Expected Return on Investment (ROI): Enter the expected annual rate of return on your investment. Typically, NPS investments have an expected ROI ranging from 8% to 10%.

- Investment Period: Enter the number of years you plan to contribute to the NPS.

- Annuity Purchase: Enter the percentage of the corpus you plan to use for purchasing an annuity. By default, this is usually set at 40%, as this is the mandatory minimum required to buy an annuity.

- Expected Annuity Rate: Enter the expected annual rate of return on the annuity. This is typically around 6% to 7%.

- Calculate:

- Click on the “Calculate” button to get the results.

Results:

- Total Corpus at Retirement:

- This is the total amount accumulated in your NPS account at the time of retirement.

- Amount Invested:

- The total amount you have invested over the years.

- Returns Earned:

- The total returns earned on your investments over the period.

- Lump Sum Amount:

- The amount you can withdraw as a lump sum at retirement (60% of the total corpus).

- Annuity Amount:

- The amount used to purchase an annuity (40% of the total corpus).

- Monthly Pension:

- The estimated monthly pension you can receive based on the annuity purchase.

Example Calculation:

Let’s go through a simple example to illustrate the calculation:

- Age: 30 years

- Monthly Contribution: ₹5,000

- Expected ROI: 9% per annum

- Investment Period: 30 years (until the age of 60)

- Annuity Purchase: 40%

- Expected Annuity Rate: 6%

Calculation Steps:

- Total Investment: ₹5,000 * 12 months * 30 years = ₹18,00,000

- Estimated Corpus at Retirement (assuming 9% ROI): This can be calculated using the future value formula for an annuity:

- FV = P * [(1 + r)^n – 1] / r

- Where P = ₹5,000, r = 9%/12 per month, n = 30*12 months

- FV = ₹5,000 * [(1 + 0.0075)^(360) – 1] / 0.0075 ≈ ₹90,00,000

- Lump Sum Amount: 60% of ₹90,00,000 = ₹54,00,000

- Annuity Purchase: 40% of ₹90,00,000 = ₹36,00,000

- Monthly Pension (assuming 6% annuity rate):

- Annual Pension = ₹36,00,000 * 6% = ₹2,16,000

- Monthly Pension = ₹2,16,000 / 12 ≈ ₹18,000

Therefore, at the age of 60, with the above assumptions, you would have a total corpus of ₹90,00,000, out of which you could withdraw ₹54,00,000 as a lump sum and receive a monthly pension of approximately ₹18,000.

Tools:

- NSDL NPS Calculator: Link to NSDL NPS Calculator

These calculations provide a basic estimate and actual results may vary based on the actual returns, changes in annuity rates, and other factors.

Payment Gateway:

- TOP 10 BEST PAYMENT GATEWAY IN INDIA (2020)

- PhonePe Payment Gateway

- PayKun – Best Payment Gateway For India 2021

- UPIGateway

- Freecharge PG

Credit Card:

- Kotak upi rupay credit card apply online

- HDFC Bank UPI RuPay Credit Card

- IDFC FIRST Power Rupay Credit Card

- PCI DSS

Banking:

- Register to IndusNet Online Banking

- BOB Kiosk Banking, BOB CSP, BC Commission chart 2024-25

- Documents Required for Opening a Current Account Online

- csc digipay lite commission 2023-2024

- DigiPay v7.3

- Airtel Payment Bank CSP

- SBI CSP Commission Structure

- SBI CSP – How to register sbi csp

- Fino CSP Lite Login

- Fino Payment Bank CSP Login

- how to apply fino payment bank csp

- Fino Payment Bank Commission 2023-2024

- Instant PIN Generation for Debit Card

- BOB CSP Browser Settings

- 7 Points on UPI Payments

- 5 Best Refer and Earn UPI Apps: Earn Free Cash Online

Other’s:

- Beyond the Beast: Jay Leno Tames the F-150 Raptor R and Unveils Its True Power

- Clash of Titans: Warriors vs. Nuggets – The Ultimate NBA Showdown Unveiled!

- United States one-dollar bill

- South Texas College – Pecan Campus

- How to disable right-clicking on a website using JavaScript?

- Unlocking Craig Brown’s Secrets to Success: The Ultimate Guide

- Unsolved Mystery: The Fate of the Five Men Aboard the Missing Titanic Tourist Submersible

- The NCAA Women’s Basketball Champion

- Dodgers

- Indian Premier League 2024

- Real-Time Billionaires

- Bernard Arnault & family

- Los Angeles Lakers

Following my social platform

| Web | www.mytechtrips.com |

| Join telegram channel | Click here |

| Join WhatsApp group | Click here |

| Click here | |

| Click here | |

| Youtube Channel 1 | Click here |

| Youtube Channel 2 | Click here |